By: Zachary Winfield

Earlier in the month, we hosted a webinar called “What Just Happened?” where we shared an industry-level analysis of the effects of the pandemic on AZA member organizations around the United States.

This analysis was completed based on data from Canopy Strategic Partners’ Audience Analytics platform, which tracks tens of millions of mobile devices all around the United States. This platform allows us to capture information about who visits facilities and when; for how long; where constituents live, work, shop, and spend time; how they identify ethnically/racially; how much they earn; the makeup of their households; and much more. The following analyses are based on data captured through this platform about the performance of 206 discrete AZA organizations based in the United States.

As a precursor to that webinar, we published the first of this two-part blog post series. If you’ve haven’t read that yet, start there!

In Part I, we answered three key questions:

- How were AZA organizations trending before the pandemic?

- How many visitors were actually lost to the pandemic?

- How have these same organizations recovered from the pandemic?

Here in Part II, we’ve gone deeper into the data to provide analysis about how geography, demographics, and population health impacted (or did not impact) recovery; and what’s been happening in the last few months as the profession continues on the road back.

Before we dive in, two quick definitions to understand:

- Pandemic Quotient is a calculation that determines how visitation changed at an organization during the height of the pandemic period (defined as Q1 2020 through Q2 2021) compared to its pre-pandemic performance.

- Recovery Quotient can be understood as a calculation that expresses to what extent visitor behavior returned to (or in many cases exceeded) pre-pandemic levels during the “recovery period,” which for the purpose of this analysis was defined as Q3 2021 through Q2 2022.

WAS THERE A GEOGRAPHIC CORRELATION?

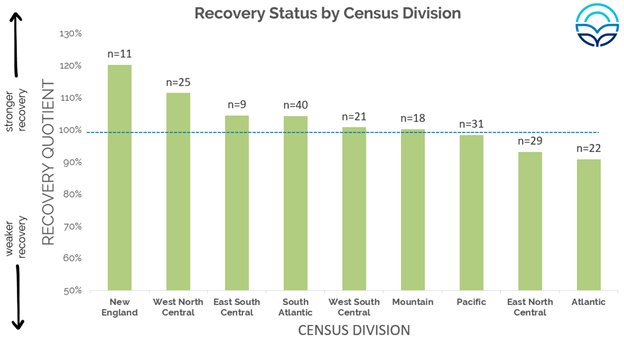

When we started digging into the numbers, the first question we asked ourselves was whether there was correlation between organizations’ physical locations and their recovery. Given the vast diversity of regional cultures and mores throughout the United States, it seemed like a good place to start. So we divided our sample of 206 AZA member organizations into nine groups as defined by their Census Divisions, which are shown here at right.

After analyzing the average recovery quotient of each respective group, we were somewhat surprised to see that there was no meaningful correlation:

Nothing about proximities between census divisions was useful at all. For example, organizations in the New England division, all the way on the left side of this chart, had the strongest overall recovery quotient. Meanwhile, those organizations in the Atlantic division, which directly abuts New England physically in the real world are all the way on the other side on the right, meaning they had the weakest overall recovery. This was initially disappointing, but we learn just as much when our hypotheses turn out to be wrong as when they are confirmed.

WAS THERE A MARKET SIZE CORRELATION?

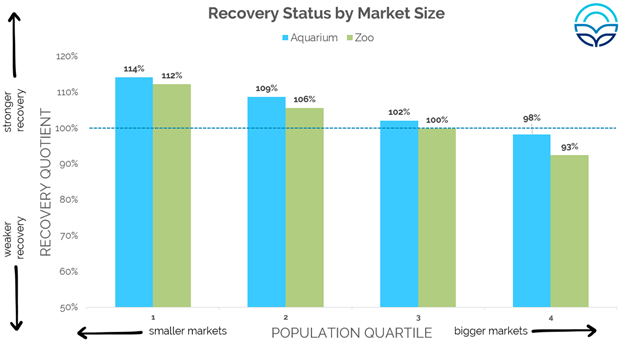

Next, we moved on to market size—we wanted to know if there was a correlation between how many people live in each market to how well they recovered. We used MSA (metropolitan statistical area) boundaries—which can generally be understood as a loose aggregation of municipalities surrounding a major economic hub—to calculate population bases, and distributed them by quartile:

Now we’re finally getting somewhere, as we did find a pretty strong correlation in this case. Those organizations on the left side of the chart (in the first quartile) are the smallest populations, the least densely populated, and in most cases, they are geographically distant from other metro areas. Those organizations had the strongest recoveries. As we move towards the right on the chart, as we get into larger and larger markets, the recovery gets weaker and weaker. This was a pretty tidy correlation even if you control for zoo versus aquarium, which we’ve done here in blue and green. It’s of course difficult to say conclusively that this is causal, but it’s well correlated.

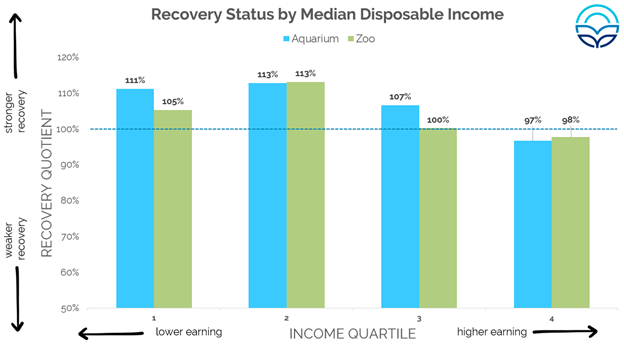

WAS THERE AN INCOME CORRELATION?

Next, we wanted to know if there was some correlation between the earning status of constituents and pandemic recovery. For that purpose, we chose the median disposal income metric, which differs from median household income in that it controls (at least to some extent) for cost-of-living fluctuations in different markets.

Again, we found there was indeed a correlation. It wasn’t quite as striking as it was with market size, but it’s clearly there. The lower earning quartiles—the first and second quartile on the left—recovered more strongly than the higher earning quartiles—the third and fourth, on the right.

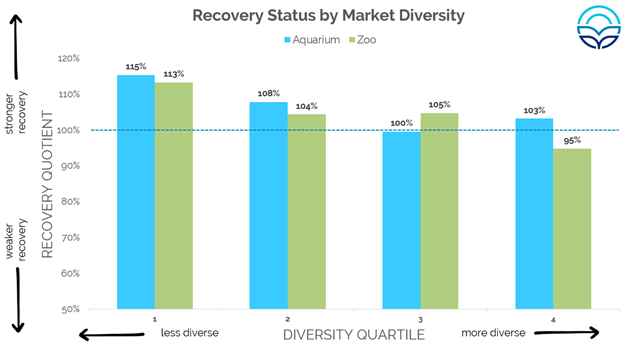

WAS THERE A DIVERSITY CORRELATION?

We then moved on to diversity. We wanted to know if there was a correlation between the diversity status of markets and their recovery status. Your first reaction might be that large markets are in aggregate going to be more diverse than the small ones, and that is true to a certain extent, but the data actually doesn’t bear it out quite as much as you might think. There are plenty of small markets with relatively high composites of diverse populations, and plenty of big markets that are less diverse than you’d expect.

But when we look at the data, we come right back to what’s now starting to look quite familiar. We have our less diverse areas on the left and moving towards the right we have higher and higher proportions of diverse populations. We observe that organizations in the less diverse markets tended to have stronger recoveries than those in the more diverse areas.

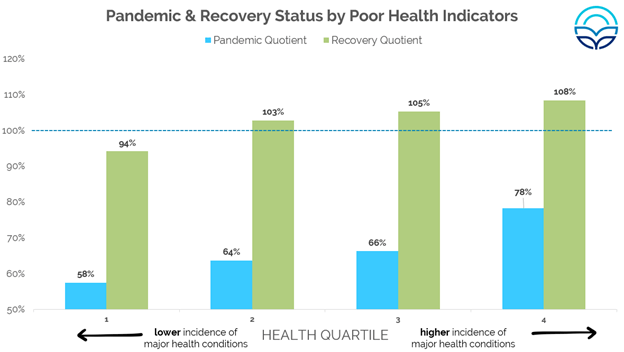

WAS THERE A HEALTH CORRELATION?

Lastly, we asked ourselves if there was some correlation between the aggregate health status of respective markets and their recoveries. This final piece of the analysis was done mostly on a lark, as we were certain, 100% certain, that markets with higher proportions of residents with serious health conditions would behave more cautiously. We were reminded again here about how amusing it is when our most visceral assumptions are wrong, and we were extremely surprised by what we learned:

On the left side of our chart are markets with lower incidence of major health issues, things like cardiovascular disease, obesity, renal disease, diabetes, cancers, and respiratory diseases. As we move to the right, those are higher incidences—much higher—the fourth quartile has about a 70% higher incidence rate than the first. And what we can see here is that in those markets which are relatively less healthy overall, not only was the recovery much stronger (the green bars) but their actual performance during the height of the pandemic (the blue bars) was also much higher.

Just to be clear, what we’re observing here is that sicker populations were more likely to patronize their local AZA organization than their healthier counterparts. We aren’t sure what to make of this finding, but you could infer that for populations who maybe weren’t all that concerned with their health before COVID, they sure weren’t going to let a pesky little once-in-a-generation deadly global pandemic stop them from getting on with their day. Very interesting, and very surprising.

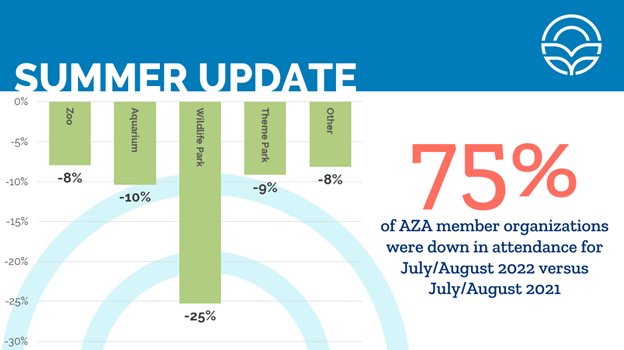

END OF SUMMER UPDATE

This analysis took a bit of time to complete, and during the interim period we heard from many of our clients and friends around the industry that they had been experiencing a softening of attendance during the middle-to-late summer months. Given that, we wanted to take a look at what we had been hearing anecdotally and test it. Here’s what we found:

The observation was not merely anecdotal. The data bore out what we had heard. During July and August of 2022, 75% of the 206 AZA member organizations in our sample were below their previous attendance levels for those same months in the previous year. While we can only speculate as to what was happening, the prevailing theory seems to indicate a confluence of two factors: the first is that the negative economic environment could be influencing spending behavior, and the second is that the huge amount of travel demand pent up in 2021 has been depleted, at least for the time being.

We hope this analysis has been interesting and useful to you, and if you’d like to learn more about how Canopy Strategic Partners’ Audience Analytics services can be a resource to you, please don’t hesitate to drop us a line.